Support CleanTechnica’s work through a Substack subscription or on Stripe.

Or support our Kickstarter campaign!

Germany’s Council of Economic Experts, working jointly with France’s Conseil d’analyse économique, has already stepped away from hydrogen as a broad energy carrier, and that shift sits uneasily alongside a 400 km pressurized segment of Germany’s hydrogen backbone with no suppliers and no customers. The joint guidance from these two economic councils was explicit on heavy road transport, one of the largest demand pillars assumed in earlier hydrogen strategies. Battery electric trucks paired with high power charging were found to be more efficient, cheaper to operate, faster to deploy, and easier to integrate into an electricity system that must expand anyway. Hydrogen refueling and supply chains were not rejected on ideological grounds, but deprioritized because they add cost, complexity, and energy losses without delivering commensurate system value.

The councils’ analysis compared entire systems rather than individual components. Battery electric trucks convert roughly three quarters of delivered electricity into motion, while hydrogen fuel cell trucks convert closer to one quarter once electrolysis, compression, distribution, and reconversion losses are included. That efficiency gap translates directly into infrastructure scale and cost. Charging requires grid reinforcement, substations, and chargers. Hydrogen requires electrolyzers, storage, compressors, pipelines or tanker trucks, refueling stations, and higher vehicle costs. On a per kilometer basis, the councils concluded that battery electric trucking is the lower cost option across energy, infrastructure, and maintenance, while also being closer to mass deployment. Their recommendation was clear. Public investment should prioritize grids and charging, with hydrogen reserved for uses where electrification is not viable. They went further, recommending the removal of hydrogen refueling station construction plans and budgets, and removal of synthetic fuels from national and EU targets.

This guidance matters because of who delivered it. Economic councils are designed to test assumptions, highlight opportunity cost, and challenge policy narratives before they harden into long lived assets. When they step away from a technology’s broad deployment, they signal that the underlying economic logic no longer holds. This was not a marginal adjustment. It removed one of the largest anticipated hydrogen demand segments from future planning.

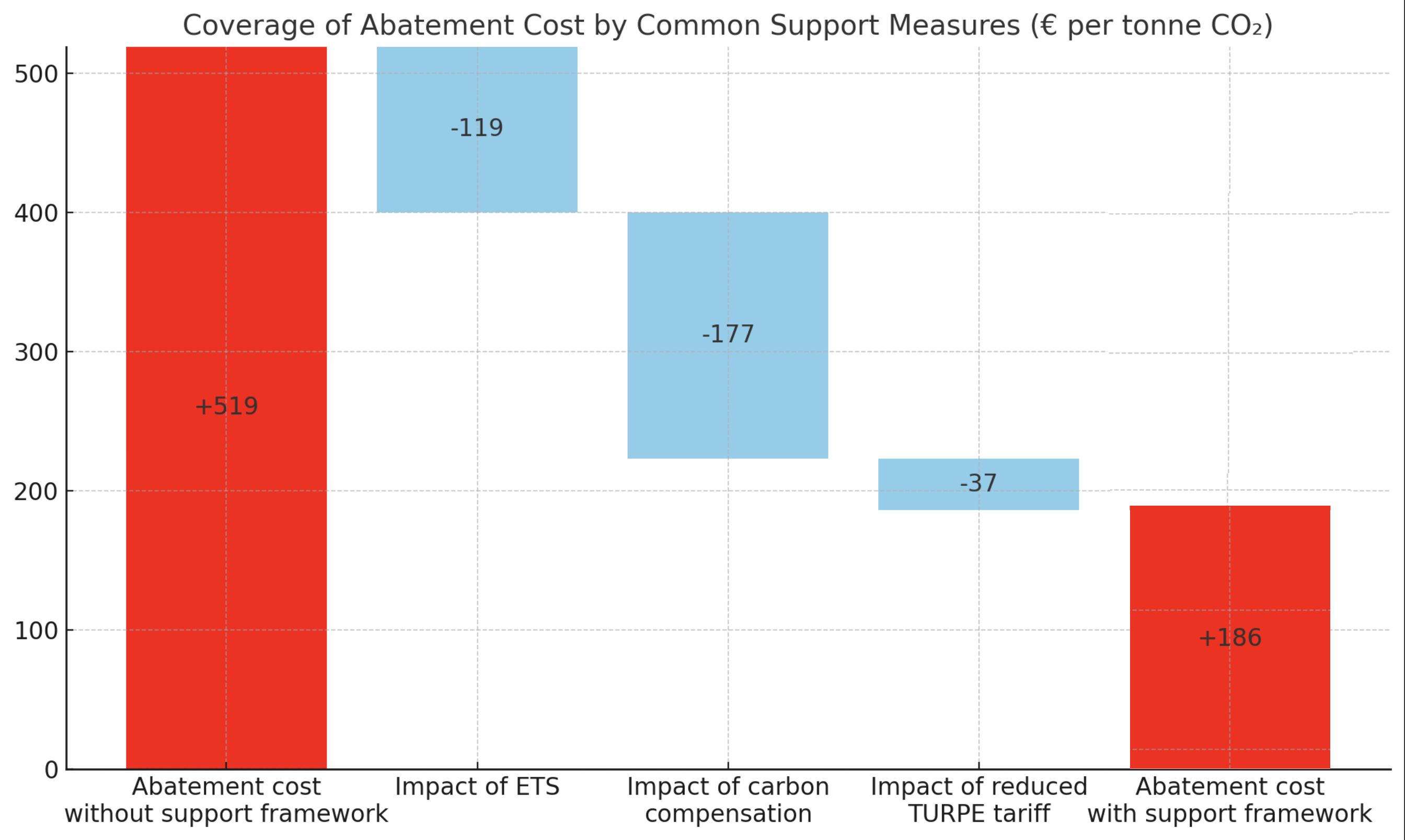

The French Court of Auditors reinforced that narrowing from a climate accounting perspective. Its assessment focused on hydrogen in transport and measured the cost per ton of CO₂ avoided when hydrogen replaces fossil fuels. The auditors traced the full chain from clean electricity through electrolysis, compression or liquefaction, distribution, and vehicle use. Across that chain, roughly two thirds of the original electricity is lost. When capital costs, operating costs, and subsidies are accounted for, the resulting abatement costs were found to be in the hundreds of euros per ton CO₂, often exceeding €400 per ton CO₂ and in some cases approaching €600 per ton CO₂. Those figures stand far above electrification alternatives that use the same electricity directly.

The Court of Auditors did not argue that hydrogen has no role. Its conclusion was narrower and more practical. In a system where clean electricity is scarce and must decarbonize multiple sectors at once, using that electricity to make hydrogen for transport delivers poor climate value compared with direct electrification. That conclusion aligns closely with the economic councils’ guidance, even though it is framed through public finance and emissions accounting rather than transport system design.

Taken together, these signals represent a structural change in Europe’s hydrogen narrative. Germany and France’s most conservative economic institutions have converged on a much narrower role for hydrogen, one that excludes broad use in transport and general energy substitution. This shift matters because it removes the legitimacy that once supported hydrogen as a default solution.

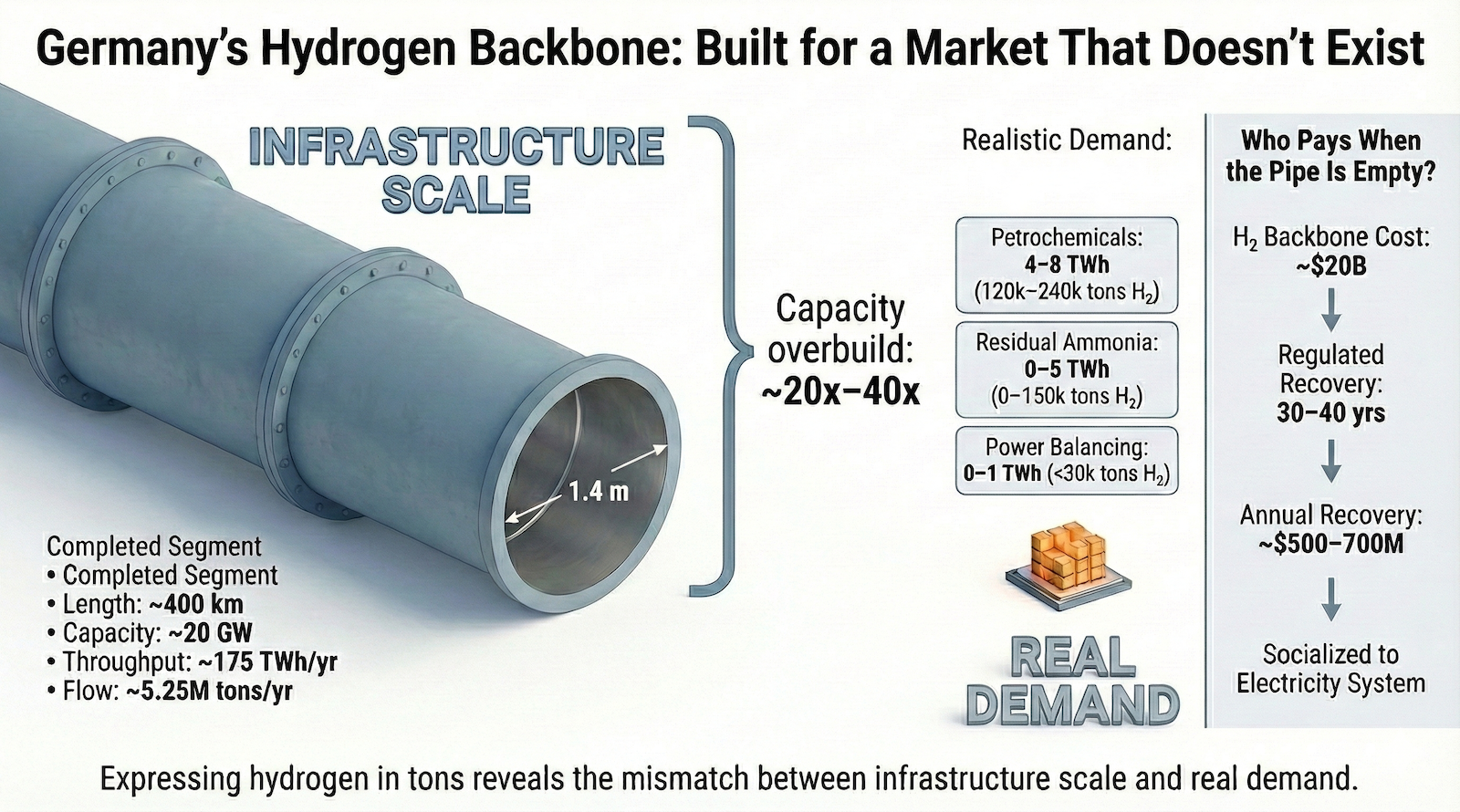

It is against this backdrop that Germany’s pressurized hydrogen backbone segment must now be understood. Hundreds of kilometers of large diameter steel pipe have been converted and filled with hydrogen. Compressors, valves, and safety systems are in place. Yet no major producers are feeding hydrogen into the system and no industrial customers are drawing molecules out. The pipeline was planned around an expansive view of hydrogen demand that included transport, heating, power balancing, and wide industrial substitution. The economic guidance from Germany and France now removes most of that demand envelope.

The backbone is not simply infrastructure waiting for time to catch up. It is a physical expression of assumptions that were widely shared when the project was conceived. Hydrogen was treated as a general purpose energy carrier whose costs would fall quickly and whose demand would scale across multiple sectors. That view was reinforced by European strategies, industrial actors seeking continuity, gas network operators repositioning assets, and models projecting favorable outcomes. Each actor acted rationally within the story as it existed at the time.

Actor network theory helps explain why the change in economic guidance has such a destabilizing effect. Actor network theory was developed in the 1980s by the French sociologist Bruno Latour, working alongside Michel Callon and John Law, to explain how technologies, institutions, and ideas succeed or fail not on their technical merits alone, but through networks of actors that reinforce one another. Originally used to study science and technology controversies, it has since been applied to energy systems, infrastructure, and policy, where narratives, models, regulations, and physical assets co-evolve and can persist long after their underlying assumptions weaken.

Energy systems are assembled through networks of ministries, regulators, utilities, industries, financiers, consultants, and analytical bodies. When these networks stabilize, their assumptions fade into the background and become difficult to challenge. Hydrogen reached that state in Europe. Cheap, abundant green hydrogen was treated as an eventual certainty rather than a hypothesis that required continuous validation. Those assumptions were in a black box at the center of network that no one bothered to open or challenge.

Within that network, economic councils and auditors occupy a special position. They do not advocate technologies or build infrastructure. They validate or invalidate the economic logic that underpins investment, opening and checking the assumptions in the black box. When they support a pathway, other actors align more easily. When they defect from the narrative, the network loosens. That is what is now happening with hydrogen as a broad energy carrier and maximalist industrial feedstock.

This loosening is not collapse. It is system learning. As electrification options mature faster than expected and electricity constraints become clearer, hydrogen shifts from default option to constrained tool. That shift improves overall system efficiency and climate impact. The tension arises because physical assets built under the earlier narrative remain in place.

The pressurized backbone is now exposed because the assumptions that justified its scale have weakened substantially. Without transport and broad energy use, the remaining hydrogen demand is smaller, more localized, and often better served by on site production or narrow regional industrial pipelines rather than long distance transmission. A national backbone sized for tens of gigawatts struggles to justify itself under that narrower future.

Continuing to defend the backbone as if the narrative has not changed carries costs. Capital tied up in underutilized infrastructure is unavailable for grid expansion, storage, industrial electrification, and efficiency measures. Workforce training focused on hydrogen operations competes with the skills needed for rapid electrification. Regulatory attention remains divided when it could be focused on the bottlenecks that now define progress. These are opportunity costs that compound over time.

A more credible role for hydrogen emerges from this reassessment. Hydrogen remains essential as a chemical feedstock in specific industrial processes. Constraining hydrogen to those roles aligns with the guidance from Germany and France’s economic institutions and improves hydrogen’s climate value rather than diminishing it.

The unresolved question is how to deal with infrastructure built under a broader story. Options include limited industrial clustering, delayed commissioning, partial repurposing, or accepting periods of underutilization. None of these are comfortable, but acknowledging the shift early reduces long term cost. An upcoming article will include my recommendations for German policy makers and strategists concerned with accelerating Germany’s transition.

Germany has the institutional capacity to manage this transition. Revising course in response to trusted economic evidence is not a retreat from ambition. It is a sign of maturity. A pressurized hydrogen pipeline with no customers is not a failure in itself. It is a marker of transition between two narratives, one expansive and one disciplined. Recognizing which narrative now governs the system is the task ahead.

Support CleanTechnica via Kickstarter

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy

cleantechnica.com

#Europes #Economic #Institutions #Step #Hydrogen

vows to fix Gravity software issues after complaints")