Support CleanTechnica’s work through a Substack subscription or on Stripe.

SunLine Transit Agency, which provides transportation for the large western California county that includes Palm Springs and Coachella, has spent a quarter century doing more than almost any transit agency in North America to try to make hydrogen buses work. It started hydrogen production and dispensing around 2000, has cycled through electrolyzers, reformers, a large PEM electrolyzer station, and now a liquid hydrogen station, and has operated or tested a long list of hydrogen vehicle types along the way. If hydrogen transit was going to mature into a durable operating model anywhere, a small desert agency with long experience, supportive regulators, and a willingness to keep rebuilding the system looked like a good candidate.

What SunLine has actually built is something more revealing and more sobering. It is not a single mature hydrogen ecosystem that has run steadily for decades. It is a chain of successive projects, upgrades, repairs, replacements, and new funding rounds, all in service of keeping a specialized fueling and vehicle system alive.

The early years matter because they show the pattern from the start. SunLine’s milestones record an 84 kg/day electrolyzer in 2000, then a 216 kg/day HyRadix auto-thermal reformer in 2004, then a commercial 228 kg/day HyRadix Adéo reformer in 2006. Alongside that fueling evolution came a rolling mix of bus technologies and suppliers. SunLine’s timeline includes the Ballard ZEbus demonstration, HCNG buses, HHICE buses, a Van Hool fuel cell bus, the American Fuel Cell Bus program, and later New Flyer fuel cell buses. That churn is not incidental. It means SunLine was not operating one stable, mature technology stack. It was participating in an extended demonstration ecosystem in which both the buses and the fueling systems kept changing.

The refueling history is best understood as four generations. The first was the early pilot electrolyzer and small demonstration fueling setup. The second was the reformer era, starting with the ATR prototype and then the commercial reformer, plus upgrades to dispensing, compression, and storage. The third was the big jump to a 900 kg/day PEM electrolyzer station completed in late 2019. The fourth was the addition of a liquid hydrogen station commissioned in 2024 to add resiliency and fueling speed to the site. That sequence is important because it shows that SunLine did not build a station in the early 2000s and then simply operate it. It rebuilt the hydrogen system over and over again as each generation proved insufficient, unreliable, or too small for the next stage of ambition.

The capital history makes the same point more sharply. Using published project figures where available and outside-view estimates where SunLine did not disclose a clean all-in number, the refueling system adds up to about $27M in 2026 dollars across the major milestones now visible in the public record. That includes the early electrolyzer, the prototype ATR reformer, the commercial SMR reformer, the 2009 compression and storage expansion, the 2011 compressor repair episode, the 2016 PSA bed and valve replacement, the 2019 PEM electrolyzer build, and the 2024 liquid hydrogen station. However one slices the details, the picture is the same. Roughly $27M of refueling capital has been spent or committed in 2026 dollars to support a hydrogen fleet that today is on the order of 31 to 32 buses.

That spending did not buy low fuel cost. SunLine’s hydrogen economics have been high and volatile for years, and the public record shows the agency knew it. NREL reported hydrogen cost at SunLine averaging $17.21/kg in the 2007 to 2008 period and explicitly said the high cost was due to low station use. Later NREL reporting showed average hydrogen cost at $26.19/kg during the 2010 to 2011 period after compressor problems. Another SunLine and NREL evaluation showed average hydrogen cost at $12.15/kg, but with monthly values ranging from $6.50/kg to $158/kg as utilization and maintenance shifted. The later PEM-electrolyzer era improved some of the economics, with NREL reporting $13.79/kg in one evaluation period, but that is still expensive fuel for transit service. The pattern is not that hydrogen got steadily cheap over time. The pattern is that hydrogen remained costly, and the cost per kilogram moved around with utilization, repairs, and station configuration. For the sake of this comparison, I normalized all costs per kg to 2026 dollar values and ensured that all had the cost of hydrogen and the amortized cost of infrastructure, as reporting varied over the years.

SunLine also had to live with the repair and reliability side of that economics. NREL documented a major compressor failure in 2011 that drove cost upward. In 2016, SunLine had to replace pressure swing adsorption bed material and a valve, and the station was down for about eight weeks while waiting for parts. During that outage, the agency brought in delivered hydrogen and limited bus service because delivered hydrogen cost more than on-site production. The transition to the 900 kg/day PEM electrolyzer did not end those issues. CARB’s final project report on that station described a rough commissioning period with 35% downtime in December 2019 alone, plus low CO2 compressor levels in the pre-cooling system, an undersized cooling system, compressor packing failure, and a heater failure in the drying system. This is not evidence of incompetence. It is evidence that hydrogen refueling remains a specialized and maintenance-heavy system even in one of the most experienced agencies on the continent.

That is one reason the liquid hydrogen station matters. The public case for it was resiliency and capacity. The California Energy Commission awarded about $5M in 2021 for a stand-alone liquid hydrogen station, and Nikkiso later said the station could fuel SunLine’s current 32-bus fleet and fill a bus in under 10 minutes. AQMD provided another million and indicated the station could fuel up to 50 fuel cell buses. Operationally, that makes sense. If the electrolyzer complex has been difficult and the fleet is larger, a truck-delivered LH2 backup and expansion path is attractive. But it is also a quiet admission that SunLine’s long pursuit of on-site hydrogen did not produce a simple, robust fueling model that could stand alone. The answer to difficult hydrogen infrastructure turned out to be more hydrogen infrastructure.

To be clear, SunLine wasn’t spending that much on the hydrogen itself through much of this. The DOE and California paid for most of the hydrogen refueling infrastructure, so the amortization of capital burden wasn’t on SunLine’s book. They likely assisted with the major refurbishment costs as well. If SunLine had been paying for its own hydrogen, it would have stopped experimenting with hydrogen long ago.

The emissions implications of that shift are not flattering. SunLine’s earlier reformer pathway was unabated SMR hydrogen, which is reasonably estimated at around 9 to 12 kg CO2e/kg H2. The current liquid hydrogen appears to be truck-delivered LH2, and I did not find public evidence that it is certified renewable. The best analytical assumption is that it is conventional fossil hydrogen that has also paid the energy and transport penalty of liquefaction and delivery. Likely they assumed that it would become green hydrogen when ARCHES built big electrolyzers. That pushes likely emissions to roughly 14 to 18 kg CO2e/kg H2. Using SunLine-specific NREL bus efficiency of 7.05 miles/kg H2 and a typical 45,000 miles per year duty cycle, each bus consumes about 6,383 kg H2 per year. A 31-bus fleet therefore uses about 197,872 kg H2 per year. At 15 to 16 kg CO2e/kg H2, that fleet emits roughly 2,968 to 3,166 tons CO2e per year.

The diesel comparison is uncomfortable for a technology often described as clean. Using a representative diesel transit bus figure of 4.14 mpg and diesel combustion emissions of about 10.21 kg CO2 per gallon, an equivalent diesel fleet running the same annual distance would emit about 3,440 tons CO2 per year. That means SunLine’s hydrogen fleet, if fueled primarily with conventional delivered LH2, is only around 8% to 14% lower in annual emissions than diesel under those assumptions. A zero-tailpipe fleet can still be a high upstream emissions fleet. SunLine’s hydrogen buses are not near-zero carbon if they are leaning on gray liquid hydrogen. They are just somewhat better than diesel while being far more capital-intensive and operationally specialized.

The contrast with battery-electric is revealing, and not in hydrogen’s favor. California’s own bus market shows that battery-electric has become the dominant zero-emission pathway. As of July 2025, CALSTART counted 1,933 battery-electric transit buses in California versus 690 fuel cell buses. My recent analysis found 2023 saw peak orders for more fuel cell buses, with significant drops in 2024 and only 15 in 2025, while battery electric buses continue to be purchased. SunLine has around 4 as well, and stated plans to grow that to 18. Tailpipe emissions for the battery electric buses charging at California’s grid intensity, are about 20% that of diesel’s, and they will be declining each year as California continues to decarbonize its grid. Remember, the point of low-emissions buses is low emissions. Battery electric delivers that. Hydrogen isn’t delivering that.

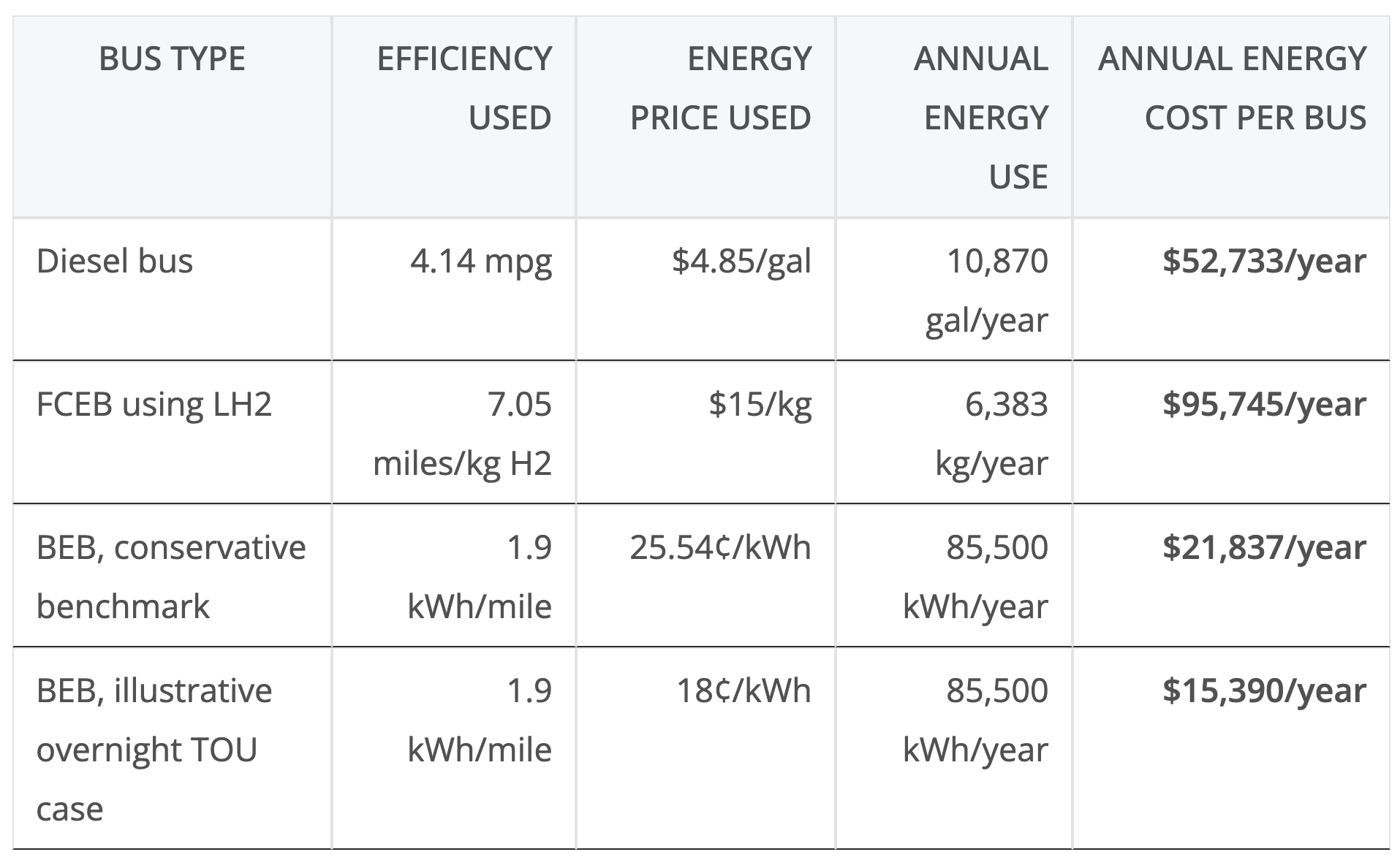

Using the same 45,000 miles per bus-year as the earlier emissions comparison, the energy-cost gap is severe. A representative diesel bus at 4.14 mpg and California’s 2025 average diesel price of about $4.85/gal comes in at roughly $52,700 per year for fuel. A fuel-cell bus at 7.05 miles/kg running on SunLine-style LH2 at about $15/kg comes in at roughly $95,700 per year. A battery-electric bus at 1.9 kWh/mile charging at California’s average commercial electricity rate of 25.54¢/kWh would cost about $21,800 per year, and at a more plausible overnight charging rate of 18¢/kWh would cost about $15,400 per year. In other words, each hydrogen bus is burning about $73,900 to $80,400 more per year in energy than a BEB covering the same distance. Across SunLine’s 31 fuel-cell buses, that implies roughly $2.29M to $2.49M more in annual energy cost than if those same 31 buses were battery-electric, before even considering the extra maintenance burden and refueling infrastructure costs that come with hydrogen.

That brings the discussion to ARCHES and the future. Hydrogen transit systems need money for buses, for fueling, for storage, for compressors, for chillers, for repairs, and eventually for replacements of specialized equipment that no diesel or battery-electric fleet manager has to think about in the same way. Foothill Transit’s 2025 board materials were the clearest example of what happens when a major funding layer disappears. DOE’s ARCHES-related support was terminated, removing $300,000 per bus, a million dollars to fix their three year old refueling station, and another $1.4 million to expand with another refueling station, while California’s HVIP program remained oversubscribed and uncertain. Staff responded by recommending a shift away from hydrogen because doing so would save about $27.6M upfront and about $1.8M per year in fuel cost. SunLine is a different agency with a longer hydrogen history, but the structural dependency is similar. Without ARCHES-scale capital support or something close to it, the next round of station overhauls, component replacements, and bus procurements becomes harder to finance.

This is the risk now hanging over SunLine’s 31 hydrogen buses. The agency has already shown that it can operate them. That is not the same as showing it can support them economically over the next decade without another major wave of outside funding. If the liquid hydrogen station becomes the preferred fueling pathway because it is simpler to operate than the electrolyzer complex, SunLine becomes more dependent on truck-delivered gray hydrogen with higher embedded emissions. If the PEM station and associated equipment continue to need fixes and upgrades, SunLine will keep needing capital. If replacement fuel cell buses remain expensive and the rest of California keeps moving toward BEBs, hydrogen bus procurement becomes harder to justify on pure economics. The likely result is not an immediate collapse. It is a grinding financial problem in which the agency is left supporting a capital-heavy, maintenance-heavy, emissions-compromised hydrogen system with fewer large grant programs willing to carry the load.

The newest and likely most durable piece of SunLine’s hydrogen system is the 2024 liquid hydrogen station, which means it is also the asset most likely to determine when the agency faces its next real strategic decision. There is no clean industry rule saying an LH2 transit station lasts a fixed number of years before major recapitalization, but the outside view is not encouraging. NREL’s hydrogen-station reliability work shows that dispenser, compressor, and chiller systems dominate maintenance events, with failure frequencies far higher than conventional fueling systems.

SunLine’s own history points the same way. Its hydrogen infrastructure has needed a meaningful rebuild, replacement, or repair cycle roughly every four to five years, moving from early electrolyzers to reformers, then through major compressor and PSA repairs, then into the PEM electrolyzer rebuild and now the liquid hydrogen station. For the LH2 station itself, the civil works and tank shell may last a decade or more, but the cryogenic pump, vaporizer train, controls, dispenser hardware, and associated balance of plant are much more likely to force a major refurbishment sooner. On that basis, the first serious recapitalization window is likely around 2029 to 2031, with 2030 the central case.

That timing matters because the 2024 LH2 station is clearly the operational backbone for SunLine’s roughly 31 hydrogen buses. If it reaches a major refurbishment point around 2030, the agency is unlikely to be looking at a minor expense. A reasonable outside-view estimate is that a midlife refresh would cost about 20% to 35% of original capex, which on the roughly $14.55M 2026-dollar station estimate implies something like $2.9M to $5.1M. A more extensive overhaul could rise into the $5.8M to $8.7M range.

If ARCHES-scale funding does not return, an outcome I consider likely now that the hydrogen hype bubble has faded globally, that is the point at which SunLine’s hydrogen future becomes much harder to defend economically. The agency would be deciding whether to put several million more into keeping a gray-hydrogen fueling system alive, with all the maintenance and supply risk that implies, or start directing that money toward a battery-electric transition with simpler infrastructure, lower operational costs and a much broader market behind it. My expectation is that SunLine will park its fleet prematurely and permanently in 2030 or 2031, as Aberdeen just did. Of course, a fully rational transit agency would have looked at the clear results of 20 years of very high costs and high actual emissions and pivoted to battery electric buses by 2019.

SunLine deserved respect for persistence and technical ambition in the 2000s. By the 2010s it was questionable what they were proving, but at least the number of buses remained a small fraction of their 140 bus fleet. It has done more than almost any transit agency to give hydrogen buses a fair trial over many years and many technology cycles. Expansion since 2019 was a strategic mistake, as that long history points to a conclusion that is difficult to avoid. Hydrogen transit at SunLine has not matured into a low-cost, low-risk, low-carbon operating model. It has remained a sequence of expensive infrastructure generations, specialized vehicle procurements, repair episodes, and policy-supported pivots in fuel supply. With ARCHES gone and no sign that hydrogen economics have crossed into self-sustaining territory, SunLine looks less like a glimpse of transit’s future and more like a well-funded case study in how hard it is to keep hydrogen buses running at all.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy

cleantechnica.com

#Gray #Hydrogen #High #Costs #Real #Emissions #SunLines #Fuel #Cell #Fleet