May saw plugin EVs at 28.5% share in Germany, up from 18.5% year-on-year. BEV volume increased by 45% year-on-year, while PHEVs grew 79%. Overall auto volume was 239,297 units, almost flat YoY. May’s best-selling BEV, for the 5th consecutive month, was the Volkswagen ID.7.

May’s sales saw combined EVs at 28.5% share in Germany, with full electrics (BEVs) at 18.0% share, and plugin hybrids (PHEVs) at 10.5%. These compare with YoY figures of 18.5% combined, 12.6% BEV and 5.9% PHEV.

The YoY baseline (May 2024) was lower than usual (still recovering from late 2023’s BEV incentive cuts), so take the apparently large YoY gains with a pinch of salt. Year-to-date cumulative plugin share is obviously much improved YoY, now standing at 27.4% (with 17.6% BEVs), compared to 18.3% (and 12.0% BEVs) in 2024. If we look further back to 2023, the YTD share stood at 20.6% (and 15.0% BEV), so two years later, Germany’s transition is moving in the right direction, even though PHEVs are playing an outsized role in the growth story.

A large part of the YoY BEV boost comes from a major change from Volkswagen Group, whose BEV volumes more than doubled YoY in May. Indeed, Volkswagen Group’s change of pace is so influential for BEV sales in its home market that fully 82% of Germany’s YoY BEV volume growth came from the group, and they sold half of all of May’s BEV. Whether this comes from a change of strategy, a change of culture, a change in supply chains, or some other reason, please let us know in the comments.

The last 3 months have each seen combined plugins (28.5% in May) take more market share than petrol-only vehicles (28.4%). This has only happened on a couple of isolated occasions in the past, but is now a regular occurrence. Partly this is due to petrol-only being also substituted by mild-hybrids, with the HEV+MHEV category also strong (28.0%). However, this hybrid category itself seems to have peaked over the last 12 months, and it looks like future substitution of petrol-only will go mainly to plugins.

Meanwhile, diesel-only sales continue to steadily fade, at a near-record low of 14.7% share, and 35,193 units in May.

Best-Selling BEV Models

For the 5th consecutive month, the Volkswagen ID.7 was the best-selling BEV in Germany, with 3,149 units registered in May. Its smaller sibling, the Volkswagen ID.3, came in second with 2,939 units, and their group cousin, the new Skoda Elroq, came third with 2,690 units. This was the new Elroq’s first time in the top 3.

The Volkswagen Group’s strength extended beyond the top three, taking the 4th to 8th ranks also, and a further 3 positions lower down in the top 20.

There weren’t many big moves in the top 20, mostly just steady progress from some of the newer models. As mentioned, the new Skoda Elroq continued its climb, reaching third. The Audi A6 e-tron also reached its highest rank, in 6th, and its sibling, the Q6 e-tron, gained 7th, also a personal best. The new Hyundai Inster climbed to 10th, with 1,122 units.

There were two debutant models in May. The new Mazda 6 BEV, a large sedan (4,921 mm), registered 8 initial units. The model is around the same length as the Volkswagen ID.7, is a modification of the existing Mazda 6 ICE vehicle, and has an MSRP starting from €44,900.

The other debutant, with just 2 units registered, was the new Toyota Urban Cruiser EV. These are testing units for now, as the European launch is not until “late 2025” according to Toyota. The specs are not yet fully confirmed, so we will come back to this once it sees its commercial launch.

In the growing class of small-and-affordable BEVs, the Hyundai Inster led with 1,122 units, with the Renault 5 seeing 406 units, and the new Opel Frontera 401 units (in just its second month). The Leapmotor T03 saw 297 units, the Citroen e-C3 279 units, and the Dacia Spring saw 202 units. April’s debutants, the BYD Dolphin Surf, and the Renault 4, saw 38 units and 7 units, respectively, in May. Most of these small models are still relatively early in their life, with production still ramping up, and juggling allocations with limited availability – let’s keep an eye on them.

Here’s the trailing 3-month chart:

Volkswagen’s ID models take the full podium, with the ID.7 leading yet again. Indeed, Volkswagen Group took 10 of the top 11 spots, a remarkable achievement.

The new Skoda Elroq has quickly overtaken its larger sibling, the Enyaq, and climbed to 4th place. Given the more accessible pricing, we can expect that pecking order to remain the norm.

The Audi A6 e-tron launched a year ago, but has recently seen volumes step up significantly, and has climbed to 7th rank – impressive considering the €62,800 starting price.

The other big climber in the top 20 was the Hyundai Inster, which had only just launched in the prior 3-month period but has quickly climbed to 11th rank – a great achievement. Further back, its larger sibling, the EV3, has also climbed steadily since launching in October. The Kia EV3 is now in 17th spot.

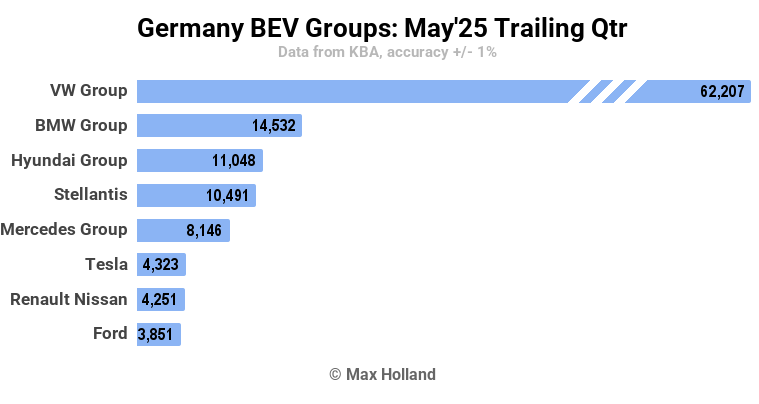

In the manufacturing group rankings, Volkswagen Group of course still leads strongly. It has increased its share of the BEV market to 47.8% over these past three months, compared to 46.3% over the prior three.

BMW Group has retained second place over the period, though with share dropping from 13.1% to 11.2%. Mercedes Group dropped from 3rd to 5th (8.2% down to 6.3%), and Hyundai Motor Group stepped up from 4th to 3rd (6.8% to 8.5%).

Perhaps most impressively, Stellantis grew share from 4.6% to 8.1%, and stepped up from 6th to 4th.

Most of the remaining ranks remained more stable, but Tesla lost share from 6.5% to 3.3% over the period. Will deliveries of the new Model Y be able to claw back much of this share? Let us know in the comments.

Outlook

Germany’s macroeconomy “recovered” to 0% YoY GDP growth in Q1 2025. This is an improvement over the previous six consecutive quarters, which were all negative.

Inflation remained stable at 2.1%, and ECB interest rates reduced from 2.4% to 2.15% in early June, which may give a lift to new car financing. Manufacturing PMI remained flat in May, at 48.3 points.

What are your thoughts on Germany’s auto market, and the EV transition? Will 2025 continue to show upward progress, after the backtracking in 2024? Which models are you looking out for, or expecting to do well? Do you know why and how Volkswagen Group has suddenly stepped up its BEV volumes over the past few months? Please share your insights and perspectives in the comments below.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Whether you have solar power or not, please complete our latest solar power survey.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy

cleantechnica.com

#EVs #Share #Germany #Volkswagen #Group #Takes #BEVs