Support CleanTechnica’s work through a Substack subscription or on Stripe.

Aberdeen’s decision to retire and try to sell its 25 hydrogen double decker buses closes a chapter that began with confident claims about global leadership in clean transport. The fleet was promoted as the world’s first hydrogen double deck operation and positioned as a foundation for a broader hydrogen economy that would anchor hundreds of local jobs. After several years of mixed performance, infrastructure strain, and parallel deployment of battery electric buses, the council chose to pivot away from hydrogen. The decision was probably cathartic for many in Aberdeen. It was arithmetic catching up with ambition.

The council has indicated that it intends to sell the 25 hydrogen double deckers to recover some capital, but the likelihood of achieving a meaningful resale value is low. There is no deep or liquid secondary market for used hydrogen buses. Previous hydrogen bus pilots in places such as British Columbia ended with vehicles being listed for sale, yet those cases did not lead to the emergence of an ongoing aftermarket. Hydrogen buses are tightly coupled to specific refuelling infrastructure, maintenance expertise, and supply contracts, which sharply limits the pool of potential buyers. Any operator considering a used hydrogen bus must already have compatible hydrogen supply and trained technicians, or be willing to build that capability for a small fleet of aging vehicles. In practice, most hydrogen deployments have been grant-supported pilots rather than commercially scaled systems, so the number of prospective purchasers is small. Aberdeen may find a buyer, but the expectation of a substantial capital recovery is optimistic given the absence of a functioning global resale market.

If the focus is strictly on hydrogen double deck buses, the used market is thin. The primary platform in operation has been the Wrightbus StreetDeck Hydroliner, deployed in limited numbers in London, Aberdeen, and Northern Ireland. London introduced an initial batch—likely due to political pressure from hydrogen-focused Lord Bamford, founder of JCB, to keep his son’s company WrightBus out of insolvency—but has not pursued follow-on orders, instead concentrating new procurement on battery electric double deckers. Belfast and Metrobus added some additional hydrogen units, but these remain small fleets rather than rapidly scaling programs. There is no evidence of a broad procurement wave of hydrogen double deck buses across the UK comparable to the steady and much larger rollout of battery electric double deckers in major cities. The technology persists solely in niche deployments, with no growth momentum that would suggest willing buyers.

The original vision was coherent within the misguided optimism of the mid 2010s. Hydrogen was widely framed as a universal energy carrier. Scotland was seeking post-oil positioning, and like many fossil fuel economies saw hydrogen as an energy carrying savior. Aberdeen had already invested in hydrogen infrastructure, including the Kittybrewster refuelling station delivered in 2015 at roughly £1 million in capital from BOC. By 2020, 15 hydrogen double deckers were delivered under an £8.3 million program supported by the Scottish Government and EU funding. Ten more followed under an additional £4.5 million award. Individual buses were around £500,000 each. The plan was that this fleet would anchor a hydrogen hub, scale into heavy vehicles, and help justify new local hydrogen production.

The economics of the refuelling station were always the critical factor. Kittybrewster was designed for about 360 kg of hydrogen per day, or roughly 131,400 kg per year at full utilization. Reported throughput suggests about 160 tons dispensed over four years, which works out to around 40,000 kg per year. That is about 30% of nameplate capacity. The 2024 council documentation recorded operating costs of approximately £974,000 over three years, or roughly £325,000 per year. Against a £1 million capital cost, that is about 30% of capex annually in O&M alone. That aligns with what I have previously calculated for California hydrogen refuelling stations, where O&M frequently lands in the 20% to 35% of capex per year range once compressors, service contracts, and staffing are included. It does not align with the 4% O&M assumptions still embedded in many transportation cost models and is another data point about the high cost of running hydrogen refueling stations.

The contrast with battery electric charging infrastructure is structural. A hydrogen refuelling station such as Kittybrewster is effectively a small industrial plant, with electrolysers that have finite stack life, high pressure compressors, drying systems, storage vessels, safety systems, and specialized dispensers. Electrolyser stacks typically require major refurbishment within a decade, compressors are maintenance intensive, and O&M can run in the 20% to 35% of capex per year range, as Aberdeen’s own numbers indicate. By comparison, a battery electric depot charging installation is primarily electrical infrastructure: grid connection upgrades, transformers, switchgear, rectifiers, and charging cabinets. There is no fuel production, no high pressure storage, and no chemical processing. Maintenance is typically a small fraction of capex, there are no stacks to replace and no compressors to overhaul, and expansion is modular and incremental as fleets grow. When a charging unit reaches end of life it is replaced as a component. When a hydrogen station reaches end of life it often requires coordinated and capital intensive reinvestment across multiple subsystems. That difference in complexity and lifecycle burden goes a long way toward explaining why one struggled to justify further capital and the other scales predictably with demand.

Annualizing the £1 million capital investment over 10 years at a 7% corporate discount rate yields about £142,000 per year. Adding the recorded £325,000 per year in O&M brings fixed annual cost to roughly £467,000. At 40,000 kg per year, fixed cost alone is about £11.70 per kg. Even if throughput were closer to 60,000 kg per year, fixed cost would still be around £7.70 per kg. Full system electricity consumption for onsite electrolysis including balance of plant and compression is about 65 kWh per kg. Using a realistic large business electricity rate in Scotland of roughly £0.205 per kWh, electricity alone costs about £13 per kg. Adding fixed cost produces hydrogen in the range of roughly £20 to £25 per kg at Kittybrewster.

The hydrogen refuelling station did not fail because of some single dramatic breakdown but because it reached the practical end of its initial operational life and required substantial reinvestment to continue operating. Kittybrewster was showing its age by the early 2020s: compressors, dispensers and the electrolysis stacks themselves were approaching the point at which major overhauls or replacements are typical in hydrogen station life-cycle plans, and the station had delivered only a fraction of its theoretical throughput because the fleet itself never created the sustained demand foreseen in early project models.

Council papers in 2024 laid out that a life-extension programme was needed to keep the station in service, but BOC, as the owner and operator, declined to invest in that capex without long-term contractual guarantees on operations and revenue from the council or its partners. From BOC’s perspective this was a business decision: without a firm committed offtake or long-term operating contract to underwrite the cost of stack replacement, compressor servicing and controls upgrades that would likely run into the low hundreds of thousands of pounds, the risk and cost were theirs to carry for uncertain future benefit. As the operating contract expired, BOC began decommissioning activities, and the station stopped regular production, leaving the hydrogen buses effectively stranded without reliable fuel. This sequence of reaching end-of-life technical requirements, absence of a clear revenue stream to justify overhaul costs, and the station ceasing to produce fuel set the stage for the council’s pivot away from hydrogen altogether.

The council considered taking ownership of the asset. Council papers in 2024 indicate that officials were exploring a transfer so that public funds could be used to refurbish and extend the station’s life, rather than investing in a privately owned facility. The logic was that if hydrogen remained part of Aberdeen’s transport strategy, the city would need direct control over its refuelling infrastructure. In practice, this would have meant the council assuming not just the capital cost of upgrades but the ongoing technical and financial risk of operating a small, under-utilized hydrogen plant.

By the time the council formally decided to dispose of the fleet, the hydrogen buses had already been effectively sidelined for a prolonged period. Reporting indicates that regular service ceased in mid to late 2024 as refuelling reliability deteriorated and production at the Kittybrewster station faltered. That means the buses sat idle for well over a year before the final policy pivot in early 2026. For a capital asset designed around a 15-year service life and roughly 1,000,000 km of operation, losing 12 to 18 months of active deployment is not a minor disruption. It represents a meaningful erosion of expected lifetime utilization and further worsens the already strained cost per km economics.

The wider hydrogen strategy in Aberdeen was tied to a larger plan for expanded refuelling capacity under a joint venture with BP, structured through a company called bp Aberdeen Hydrogen Energy Limited. That project had moved well beyond conceptual stages: the council approved seed funding, planning permission was granted for a new hydrogen production and refuelling facility at Hareness Road linked to a solar farm on the former Ness landfill, and a phased build was envisaged that would produce over 800 kg of hydrogen per day in its first phase with capacity to grow to multiple tonnes as demand expanded.

The narrative supporting that plan rested on the assumption that the city’s own hydrogen double-deck fleet and other future hydrogen vehicles would create predictable demand, justifying both the capital investment and the long-term operating commitments. Kittybrewster was phase one, BP’s facility was supposed to replace it as phase 2 and there were expectations of a phase 3 with shipping and aviation fuels. With the collapse of hydrogen as a viable bus solution and no other large, committed offtake on the horizon, the council is now actively seeking to unwind or exit its obligations in the joint venture rather than proceed with building out the hub. What was once sold as an economic opportunity and regional anchor project has become a liability of uncertain value precisely because the foundational demand assumptions have evaporated.

Aberdeen City Council faces real financial and contractual exposure as it seeks to unwind its joint venture with BP over the planned hydrogen production hub, which had been budgeted at around £20 million for the first phase of build-out. Officials are understood to be in negotiations on how to transfer or terminate the partnership rather than simply walk away, which could involve bearing costs tied to planning, site preparation, permitting and early project development that BP and the council had already committed to under the joint venture agreement.

Because BP made a final investment decision in mid-2024 and the venture had progressed toward construction before being paused, the council may also need to address sunk costs it agreed to under JV funding arrangements as well as any liabilities for commitments made to third parties or contractors. In discussions reported between the council and BP, part of the exit planning appears to involve negotiating the transfer of the joint venture entity back to the council so that assets and obligations can be managed in a way that aligns with the pivot to battery electric infrastructure, but this transfer itself is likely to carry accounting and cash implications for Aberdeen’s balance sheet and future capital programmes.

This set of ongoing fiscal liabilities after the end of attempts to grow hydrogen fleets is typical as well. My guidance piece for transit agencies expecting to receive hydrogen buses around a risk mitigation workshop makes it clear that cities and agencies need to carefully plan for failure to avoid being left on the hook.

It is also worth remembering that the hydrogen double deck fleet was not Aberdeen’s first attempt at hydrogen buses. Between 2015 and about 2020 the city operated ten Van Hool A330H single deck hydrogen buses as part of the original Aberdeen Hydrogen Bus Project. Those vehicles were fuelled at the Kittybrewster station and ran in regular service for roughly five years under a publicly funded demonstration program. When that phase ended, the buses were withdrawn rather than forming the foundation of a growing commercial fleet. At least one entered museum preservation, and there is no evidence of a meaningful secondary market or redeployment elsewhere. In other words, Aberdeen had already completed a full hydrogen bus trial with Van Hool single deckers before committing to 25 new double deckers. Those buses cost about €850,00, vastly higher than any buses, but were apparently fully funded by the EU Jive program before being abandoned. One went into a museum and the rest apparently were scrapped. The second phase was not a first experiment. It was a renewed bet on a technology that had already been tested locally and had not scaled organically.

As a reminder, Van Hool was one of the early European manufacturers to make a significant strategic bet on hydrogen fuel cell buses, positioning models such as the A330H as part of a zero-emission future well before battery electric buses had matured. That bet coincided with other strategic strains, including aggressive expansion, exposure to low-margin contracts, and supply chain disruptions in the early 2020s. By 2024 the company entered bankruptcy proceedings, and its assets were split between new owners, with the bus division effectively carved up rather than continuing as a unified manufacturer. The hydrogen focus was not the sole cause of its collapse, but it was part of a portfolio of high-risk bets in a market that shifted rapidly toward battery electric. At the same time, Dutch transit authorities that had once explored hydrogen for regional buses increasingly pivoted to battery electric fleets, citing cost, infrastructure simplicity, and reliability. The Netherlands, long considered open to hydrogen in mobility, has in practice moved decisively toward electrification for urban and regional bus transit, reinforcing the broader European trend away from hydrogen buses at scale.

Van Hool is far from alone in OEMs which have committed to hydrogen drive trains entering insolvency. The number of entrants which still offer hydrogen vehicles is overtopped by the ones that have exited the market or gone bankrupt. Quantron, Nikola and Hyzon are higher profile failures, but far from the only ones.

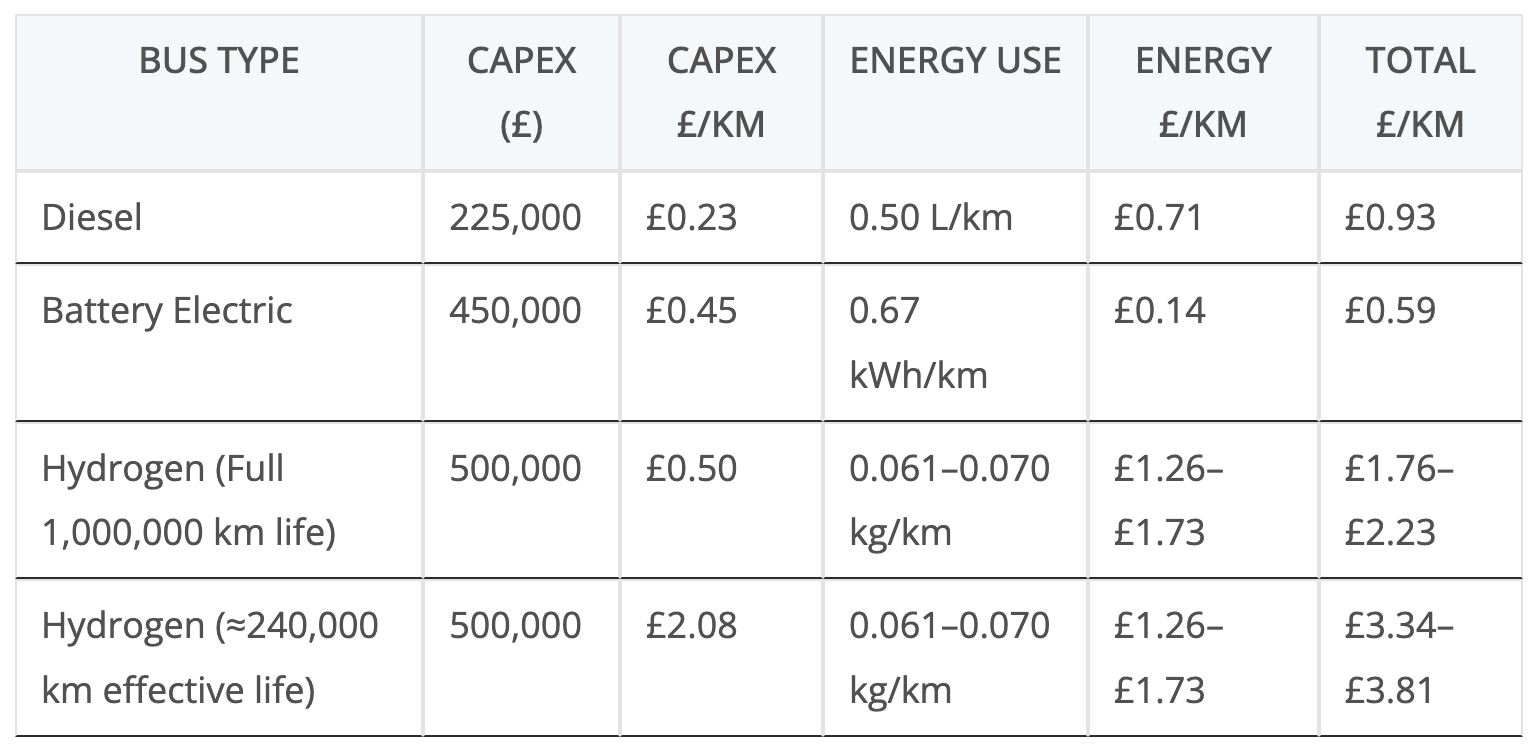

When translated into cost per kilometre, the picture becomes clearer. Hydrogen double deck buses typically consume about 6 to 7 kg per 100 km, or 0.06 to 0.07 kg per km. At £22 per kg midpoint, that is around £1.32 to £1.54 per km in energy. Using the upper end of the cost range pushes that to around £1.70 per km. Diesel double deckers typically consume about 0.5 litres per km. At roughly £1.42 per litre, fuel cost is around £0.71 per km. Battery electric double deckers such as the Enviro400EV consume about 0.67 kWh per km. At £0.205 per kWh, electricity cost is about £0.14 per km. On energy alone, hydrogen is roughly 2 to 4 times the cost of diesel and about 10 times the cost of battery electric in Aberdeen’s context.

Looking at full lifetime capital and energy costs reinforces the gap. Assuming a 1,000,000 km service life, capital cost per km for a £500,000 hydrogen bus is £0.50 per km. Diesel buses at roughly £225,000 land at about £0.23 per km. Battery electric buses at around £450,000 are about £0.45 per km. Adding energy cost produces totals of roughly £0.93 per km for diesel, about £0.59 per km for battery electric, and between £1.76 and £2.23 per km for hydrogen.

However, the Aberdeen hydrogen buses did not achieve anything close to a full design life. If they effectively delivered on the order of 240,000 km before being sidelined, capital cost alone rises to about £2.08 per km, pushing total cost into the £3.34 to £3.81 per km range before maintenance and infrastructure are considered. This kind of foreshortened life is not unusual in hydrogen bus trials globally, where reliability, refuelling constraints, and policy pivots often prevent fleets from reaching their theoretical lifetime. Even under generous full-life assumptions hydrogen struggles to compete. Under real-world outcomes, the economics deteriorate further.

Infrastructure scale compounded the risk. Hydrogen stations are dominated by fixed cost. Low utilization drives up cost per kg. Kittybrewster was running at roughly 30% of capacity. The proposed BP hydrogen hub was designed to produce more than 800 kg per day in its first phase, more than double Kittybrewster’s capacity. That expansion assumed growth in hydrogen vehicles. Instead, hydrogen heavy vehicles did not scale in meaningful numbers. The bus fleet remained the primary demand anchor. Scaling supply without scaling demand increases financial exposure. The math does not improve because policy hopes it will.

Operational complexity added further friction. First Aberdeen was managing diesel, battery electric, and hydrogen buses in the same depot environment. Each drivetrain requires different skills, tools, parts, and safety procedures. Hydrogen adds high pressure storage, fuel cell stacks, and additional cooling systems. In the guidance I prepared for a hydrogen risk mitigation workshop for transit agencies, I explicitly recommended retaining diesel buses past their expected end of life as contingency cover for hydrogen reliability issues. Aberdeen effectively followed that pattern, borrowing diesel buses when hydrogen units were withdrawn. Maintaining three drivetrain technologies increases cost and complexity. It does not make failure inevitable, but it reduces resilience.

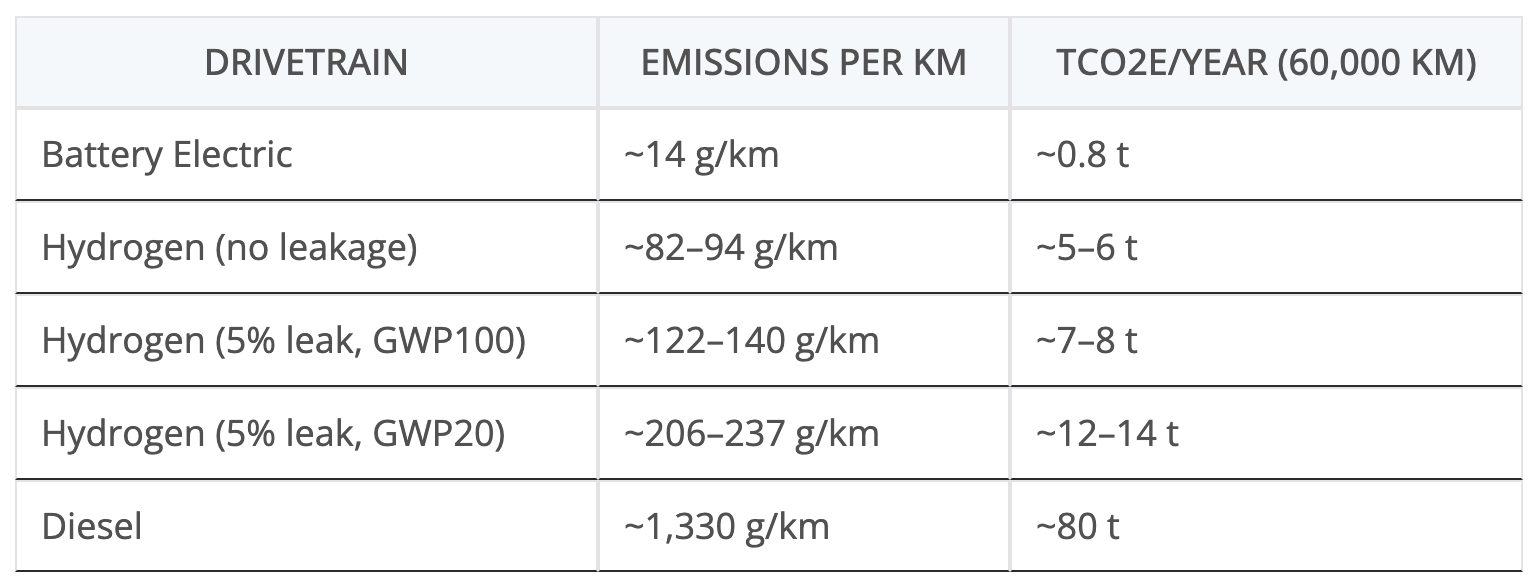

On operational emissions alone, the contrast between the three drivetrains is stark even on Scotland’s relatively clean grid. Using Scotland’s average electricity carbon intensity of about 20.7 gCO2e/kWh, a battery electric double deck consuming roughly 0.67 kWh/km emits about 14 gCO2e per km, or about 0.8 tCO2e per year at 60,000 km. A diesel double deck consuming about 0.5 litres per km at 2.66 kgCO2e per litre emits roughly 1.33 kgCO2e per km, which is close to 80 tCO2e per year over the same distance. A hydrogen bus supplied by onsite electrolysis using about 65 kWh/kg and consuming 6.1 to 7.0 kg per 100 km lands around 5 to 6 tCO2e per year on a no-leakage basis. However, assuming 5% hydrogen leakage, a reasonable assumption based on leakage data from hydrogen infrastructure leakage studies, and applying a GWP20 of about 37, total operational impact rises to roughly 12 to 14 tCO2e per year. Even on a low-carbon grid, hydrogen sits an order of magnitude above battery electric and far below diesel, but leakage meaningfully narrows the gap.

This outcome is not isolated. Brussels abandoned its hydrogen bus trial after confronting high fuel cost and supply challenges. Whistler abandoned its fleet as soon as it could, four years in. Several other European hydrogen bus programs have scaled back or pivoted to battery electric. In the UK, hydrogen fleets have struggled with availability and refuelling reliability. Beijing’s Winter Olympic hydrogen refueling stations and bus fleet are increasingly fenced off, parked and infiltrated with vegetation. Globally, hydrogen bus deployments have plateaued while battery electric bus registrations continue to grow. The pattern is visible across jurisdictions.

The predictability rests on energy conversion physics. Hydrogen for buses requires electricity to run electrolysis at roughly 65% efficiency. Compression and storage add additional losses. Fuel cells convert hydrogen back into electricity at roughly 50% to 60% efficiency. The overall round trip from grid to wheels is often below 35%. Battery electric buses move electricity from grid to wheels at above 80% efficiency. Each additional conversion step adds cost. When electricity prices are high, those losses are magnified.

Aberdeen had access to these numbers before the buses were purchased. They had already trialed hydrogen buses and refueled them. The cost structure of hydrogen refuelling stations was not hidden. O&M burdens well above 20% of capex per year were visible in California and other markets, in addition to their own experience. Multiple hydrogen bus trials had already struggled or been curtailed globally. The choice to proceed was a deliberate policy decision. The only unambiguous positive development in this story is the decision to retire the hydrogen bus fleet and pivot to battery electric. It is appropriate to acknowledge the correction, not the initial error.

The broader lesson is straightforward. Urban buses are an electron problem. They operate on fixed routes, return to depots nightly, and can charge on predictable schedules. In motion charging is simple and solves key route and elevation concerns. Hydrogen has roles in fertilizer production, refining, and certain industrial heat applications where molecules are required. Using hydrogen for urban buses competes directly with battery electric systems that are simpler and cheaper. When the energy cost difference exceeds £1 per km, subsidies can delay adjustment but cannot close the gap.

All required pilot projects have already been conducted. Aberdeen ran one. Brussels ran one. California ran many. The results converge. High fixed infrastructure cost, high O&M, low utilization, expensive fuel, and eventual transition to battery electric. Demonstrations are valuable when uncertainty is high. In this case, uncertainty has been replaced by repetition. The energy transition will be shaped by technologies that scale economically, not by technologies that require persistent subsidy to compete.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy

cleantechnica.com

#Bites #Dust #Aberdeens #Hydrogen #Bus #Fleet #Ends #Failure

")